Tag: Foreign Investment Indonesia

-

Service Level Auditing in Indonesia: How a Measured Standard Becomes a Competitive Position

Every enterprise believes it knows its own standard, and an unmeasured standard drifts until a guest sees the gap. A service level audit measures the standard an enterprise delivers against the one its market expects. This article shows, through an anonymised resort that measured too late, why a measured standard is a competitive position in…

-

Raising Growth Capital in Indonesia: The Decision That Converts a PT PMDN to a PT PMA

A growing enterprise reaches a point where its own cash cannot fund the next stage. The source of the capital it raises decides the company’s legal identity, because any foreign shareholding converts a PT PMDN to a PT PMA. This article sets out raising growth capital in Indonesia, the regime conversion brings, the sector and…

-

Brands Built to Multiply: How an Indonesian Enterprise Scales Without Parting With Capital or Control

An enterprise that builds each outlet on its own capital grows only as fast as its capital allows. A model designed to multiply lets other operators fund the growth while the owner keeps the brand and the control. This article sets out scaling a business in Indonesia through licensing, and the graduation to franchising when…

-

Supply Chain Control in Indonesia: How a Domestic Operator Secures Its Place in a Foreign Joint Venture

TraceWorthy designed a beverage network as a joint venture, with domestic capital owning farming and manufacturing and foreign capital owning distribution, and the intellectual property split so that neither side can run the business without the other. This article shows how supply chain control in Indonesia secures the domestic partner’s place.

-

Most Operators Compete by Doing the Same Thing as Their Rivals: Slightly Better or Slightly Cheaper

A foreign-owned investor came to Bali with a recycling model that could not fit the island’s roads, and left rather than adapt it. The demand stayed where it was. This article shows how a domestic enterprise finds the market gap a foreign operator leaves, and takes the position at the scale it chooses to serve.

-

Competitive Advantage in Indonesia: Winning the Position Your Rivals Cannot See

A foreign investor or partner assesses an Indonesian company across four areas before committing, namely governance, financial records, ownership structure, and communication. This article sets out what those parties require, and how a compliant domestic enterprise that meets the standard can attract capital and trade on its own terms as Bali tightens the rules on…

-

The Rise of PT PMDN, or the Return of Nominee Arrangements?

Bali’s restriction on foreign-owned companies has raised a fair question: stronger local business, or a return of nominee arrangements? The two are not opposites, and the channel the question overlooks is a lawful relationship between a foreign-owned company and an Indonesian-owned company. The Indonesian party owns the asset; the foreign company supplies services for a…

-

PT PMA Restrictions in Bali: Why the Property Workarounds No Longer Work

Bali now blocks new foreign-owned company registrations in low and medium-low risk classifications, and the familiar workarounds no longer escape it. Switching to an accommodation code meets building-footprint and reserved-field limits. The fee-based management code reserves the broker role to Indonesian citizens. Nominee structures meet beneficial ownership disclosure. Each closure carries its own verification mechanism.

-

Invoicing Offshore Clients from a Company in Indonesia

The framework for invoicing offshore clients from a PT PMA in Indonesia: the PMK 32/PMK.010/2019 zero-rated VAT regime, corporate income tax at 22 per cent on worldwide income, Article 24 foreign tax credit, LLD reporting, and transfer pricing exposure under PMK 172/2023.

-

What it Costs to Put an Employee on the Books in Indonesia

The headline gross salary is rarely the figure that arrives in a foreign owner’s monthly budget. After BPJS contributions, PPh Article 21 withholding, the THR reserve, and the payroll cycle costs, the fully-loaded cost of an Indonesian employee runs at 115 to 118 per cent of gross.

-

Taking Money Out of a Company: Dividends, Fees, Salary and Shareholder Loans

Four routes for extracting cash from a foreign-owned PT PMA: director salary, fees, dividends, and shareholder loan repayments. Worked tax comparisons with treaty rate examples on each. (185)

-

Anti-Money Laundering Compliance for a PT PMA in Indonesia

AML compliance for a PT PMA sits alongside tax and forex in every outbound transfer decision. Indonesia’s full FATF membership from October 2023, PPATK reporting under Law 8/2010, sanctions screening, and beneficial ownership disclosure.

-

Sending Money Offshore: Outbound Payments from a PT PMA

A foreign-owned PT PMA sends money offshore regularly: payments to suppliers, consultants, parent companies, and shareholders. Each transfer carries an Indonesian withholding obligation under PPh Article 26, a treaty rate application process, a Bank Indonesia reporting requirement, and a bank documentation set.

-

Consultant Tax in Indonesia: PPh Article 23 and the Consultant-Employee Line

New foreign-owned PT PMAs frequently make a recurring error: paying the full consultant invoice without applying the withholding. This article works through the PPh Article 23 framework, the seven-factor consultant-employee substance test, the 2 or 4 per cent rate structure, and the NPWP rule.

-

The Villa Question and the Line on Directors’ Personal Expenses

The villa question reaches nearly every foreign director running a Bali PT PMA in the first six months of trading. The 2023 reform to Indonesia’s benefit-in-kind regime under PMK 66/PMK.03/2023 changed the answer materially. Worked arithmetic on villa rent, vehicles, school fees, and KITAS costs.

-

The IDR 10 Billion Question: Paid-Up Capital for a PT PMA in Indonesia

The IDR 10,000,000,000 paid-up capital requirement is the entry point for a PT PMA. The figure is recorded in the company’s bank account, retained for at least 12 months under Article 27 of BKPM Regulation No. 5 of 2025, and deployed into the licensed business activity over the multi-year investment plan that BKPM measures through…

-

A Financial Reporting System that Survives Deadline Season

For a PT PMA, the Indonesian reporting year fills a calendar with deadlines that run through every month, with the quarterly LKPM and the annual cycle overlaid. The financial reporting system that prepares each filing from the company’s own records, in advance of every date, is what survives deadline season. TraceWorthy’s financial services team performs…

-

The Investment Activity Report, and Why it Exists

Every PT PMA files the investment activity report (LKPM) each quarter from the day its NIB is issued, including quarters with no activity. The 15th-of-the-month deadlines under BKPM Regulation No. 5 of 2025 set a fixed rhythm. The work behind each report falls across investment plan structuring, quarterly preparation, cross-system reconciliation, and sanctions response.

-

Why a PT PMA Pays the Same Corporate Income Tax as a Local Company

Corporate income tax in Indonesia is 22 per cent for every resident company, and a PT PMA is resident, so a foreign-owned company pays the same rate as a local one. Reliefs follow turnover and listing. Ownership reaches the position only through the withholding on dividends sent abroad and the global minimum tax on large…

-

Why a PT PMA Carries the Large Enterprise Classification

A foreign-owned company in Indonesia is classified as a large enterprise once its declared investment plan exceeds ten billion Rupiah. The label follows the size of the investment and reaches domestic companies of the same scale. This article sets out the threshold, the consequences for a foreign owner, and the policy behind the size rule.

-

Reporting Obligations: The Indonesian Company Reporting Year Mapped

A new foreign-owned company in Indonesia faces a reporting schedule that feels relentless in its first year. Almost all of it flows from general company and tax law and binds every limited liability company equally. The full reporting year is now mapped here, tracing each PT PMA reporting obligation to its instrument, authority and deadline.

-

Bali Property in 2026: Perda No. 4 of 2026, the Nominee Prohibition, and the Compliant Investment Structure

Nominee land arrangements in Bali have been void under Indonesian law since 1960. Bali Provincial Regulation No. 4 of 2026 did not create a new prohibition — it added criminal prosecution for both parties to the arrangement and for any intermediary or facilitator. The compliant structure, the risks, and the due diligence requirements are addressed…

-

PT PMA Establishment 2026: Pre-Formation Framework for Bali-Based Enterprises

Forming a PT PMA in Bali in 2026 is still viable. The OSS restriction on all low and medium-low risk KBLI classifications for Bali-address companies has raised the pre-formation due diligence requirement significantly. KBLI selection, Positive Investment List verification, physical address confirmation, and capital planning must all be resolved before a notary is engaged.

-

PT PMA Compliance 2026: What Existing Bali-Based KBLI Holders Need to Know and Do Before 18 June

Your existing PT PMA licence in Bali is valid and will not be retrospectively cancelled. The compliance obligations that do apply — four OSS trigger points, the KBLI 2025 migration deadline, a substance-based enforcement programme, and LKPM reporting requirements — require assessment before 18 June 2026. This article sets out the action sequence.

-

PT PMA Regulations 2026: What Every Bali-Based Foreign Investor Needs to Know

If you have a PT PMA in Bali, or are planning to establish one, 2026 has introduced restrictions that require review before any OSS action is taken. This article covers the Governor’s KBLI letter, the DPMPTSP’s formal proposal to BKPM, Perda No. 4 of 2026, and the 18 June migration deadline.

-

Property Acquisition in Bali: A Due Diligence Framework for Foreign Nationals

Foreign nationals acquiring residential property in Bali encounter a transaction environment that differs materially from the legal frameworks of their home countries. The protections that function automatically elsewhere, covering independent legal representation, registered easements, title insurance, and structured conveyancing, must be specifically commissioned here. This article covers thirteen due diligence categories that every foreign national…

-

Indonesia Residence Pathways: A Decision Framework for Foreign Nationals Planning Long-Term Stays

Indonesia’s residence permit system provides nine KITAS pathways, each with distinct eligibility conditions, work authorisation rules, sponsor requirements, and a different route to KITAP. The right pathway depends on the purpose of the stay and the visa the applicant is travelling on when they engage TraceWorthy. This article presents the comparison table and describes the…

-

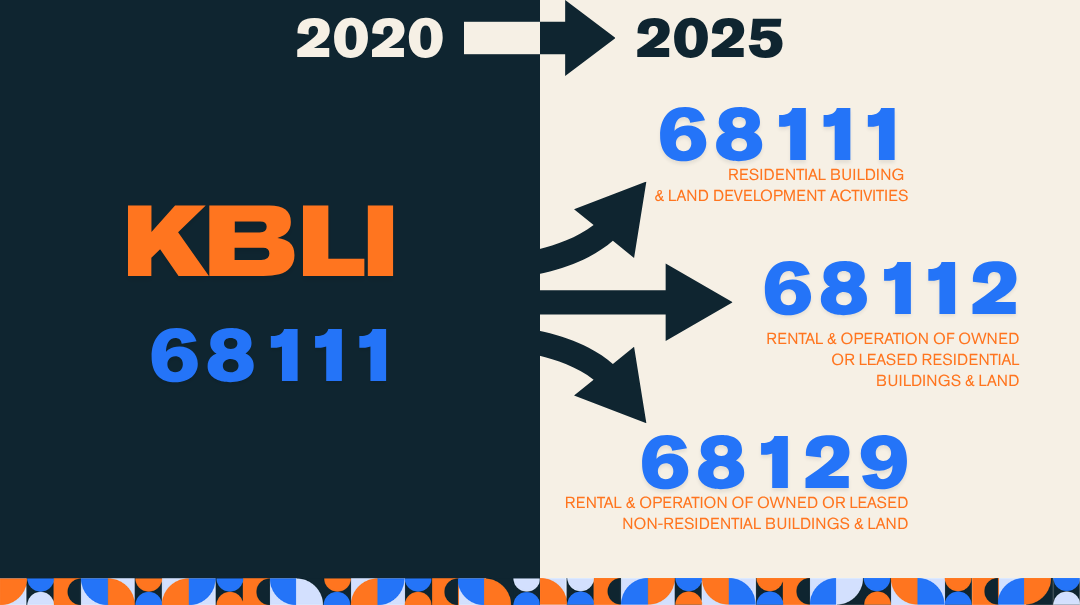

KBLI 2025: The Classification Migration Every PT PMA Must Complete by 18 June 2026

BPS Regulation No. 7 of 2025 requires every entity operating in Indonesia to align its registered business classification with the KBLI 2025 framework by 18 June 2026. For PT PMA entities whose KBLI 2020 codes split into multiple 2025 codes, the migration requires an investment threshold assessment, a foreign investment status review, and in some…

-

Annual Report Obligation: What Permenkum 49/2025 Now Requires Every PT to Prepare, Present, and Register

Permenkum 49/2025 came into force on 17 December 2025 and converts the PT PMA annual report from an informally managed governance formality into a compliance obligation with defined deadlines, mandatory SABH system registration, and sanctions that suspend access to Indonesia’s corporate filing system. For calendar-year companies, the deadline for the 2025 fiscal year is 30…

-

Investment Activity Report: LKPM Obligations, Deadlines, and the Consequences of Non-Submission

Every PT PMA in Indonesia must file the LKPM, the Investment Activity Report, every quarter from the day its NIB is issued, including quarters with no activity. The report confirms that declared investment is being realised. Missing a deadline escalates from a written warning to NIB revocation, and blocks corporate amendments through OSS in the…

-

Operating Layer: Back-Office Infrastructure, Compliance Governance, and the Cost of the Gap

TraceWorthy’s services are used by other consulting firms and real estate agencies across Indonesia, delivered to their clients under those firms’ own names. The advisory capability is available directly. This article maps the financial management, tax, land transaction, corporate structure, licensing, workplace compliance, and immigration failures TraceWorthy is routinely engaged to remedy in Bali’s operating…

-

Clean by Design: Water Treatment, Refill, and Wastewater Enterprises in Indonesia

Bali’s aquifers have lost over 50 metres of groundwater depth in some areas in less than ten years. Wastewater infrastructure on the island processes less than ten per cent of the waste it generates. The average tourist uses between 2,000 and 4,000 litres of water per day. Water treatment investment in Indonesia addresses those pressures…

-

Built to Scale: Sports and Recreation Investment in Indonesia

Indonesia’s sports economy is projected to reach IDR 43 to 45 trillion in 2026, growing at 5 to 7 per cent annually from the confirmed 2024 baseline of IDR 39.5 trillion. Padel recorded a 1,684 per cent increase in tracked activities in Indonesia in 2025, with over 1,580 new courts built during the same period.…

-

Teaching Without Permission: Lawful Entry into Indonesia’s Education and Skill-Transfer Sector

Indonesia’s total education market is valued at USD 50 billion, with the EdTech segment growing at a compound annual growth rate of 11.79 per cent. The demand environment for language training, corporate professional development, children’s enrichment, executive education, and vocational training in Indonesia is commercially confirmed. The compliance structure required to operate lawfully within it…

-

From Ingredient to Invoice: Food and Beverage Production as a Foreign Investment in Indonesia

Indonesia’s food market is valued at USD 255.38 billion in 2025, and the F&B sector contributed IDR 1,531.4 trillion to national GDP in 2024. Foreign investment in food manufacturing reached USD 3.46 billion by year-end. The sector rewards investment. It also requires a precisely sequenced compliance chain that runs from KBLI classification through BPOM registration,…

-

Beyond Tourism: The Blue Economy in Indonesia – Marine and Fisheries Investment

Indonesia is the world’s second largest aquaculture producer, with 17,504 islands and 6.4 million square kilometres of sea area. The KKP has set a marine and fisheries sector investment target of IDR 14.47 trillion for 2026, as part of a five-year programme targeting IDR 79.21 trillion by 2029. Government Regulation 78 of 2019 provides a…

-

Beyond Beach Clubs: Creative Production, Events, and Destination Experiences as Foreign Investment in Indonesia

Indonesia’s creative economy became a named licensing sector under Government Regulation 28 of 2025, for the first time placing event production, destination experiences, film and music production, performing arts, and creative education within a defined regulatory framework with its own licensing treatment and supervisory authority. For a foreign investor, this means the KBLI 2025 classification…

-

Beyond Bali: Infrastructure and Built-Environment Services as Foreign Investment in Indonesia

Indonesia’s Rencana Pembangunan Jangka Menengah Nasional 2025 to 2029 requires IDR 47,587.3 trillion in infrastructure investment. The Ministry of Public Works budget was cut 73 per cent in 2025. The gap between what the state needs and what it can fund is the commercial context in which built-environment services in Indonesia operate. This article examines…