Many owners we work with have the same experience. The business is profitable on paper, the order book is full, the team is busy, and the bank balance is still tight at the end of every month. The profit is genuine, and the cash to act on it is somewhere else.

That somewhere else is usually money that belongs to the business, in .one form or another. It is the balance kept in the account for safety, the money customers owe you, on unpaid invoices, the value tied up in stock that has not sold, and the deposits paid to suppliers ahead of need. Each of these is money, and each one has a price while it stays where it is. That price is rarely shown on any report, which is why we call it the hidden price of idle cash and slow-paying customers.

This article explains what money costs and what it could earn, in plain terms, so you can see where your own money is put to use and where it is left idle. The examples are illustrative. The judgement for your own business is work our team does with you, reading your numbers rather than a general rule.

What money costs, and what it could earn

Money has two prices, and most reports show neither. The first price is what it costs to obtain. For borrowed money that is the interest rate on the loan. For your own capital it is the return you require to justify committing it, rather than keeping it elsewhere. The second price is the opportunity cost, the lens that prices any use of money against its next best alternative. The two come together whenever you weigh what a use of money returns against what it costs and against what else the money could do.

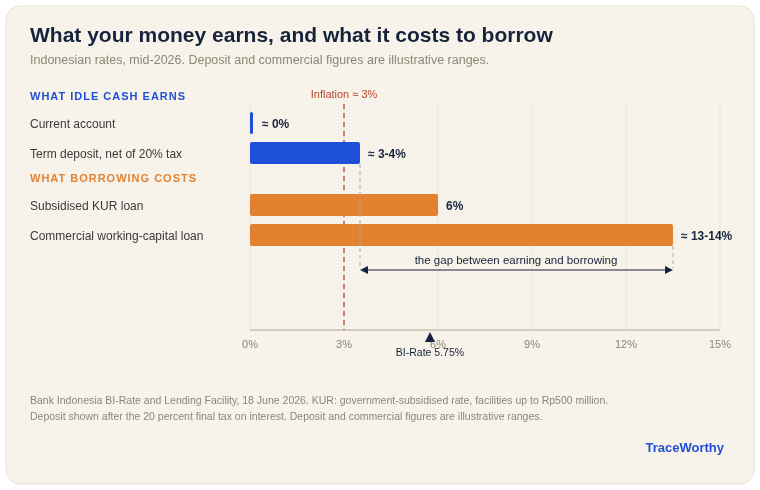

The cost of borrowing in Indonesia is easy to read at the moment. The Bank Indonesia policy rate, the BI-Rate, is 5.75 percent as of 18 June 2026, and it moved several times through the year, so any figure needs a date. A subsidised Kredit Usaha Rakyat (KUR, People’s Business Credit) loan is set at 6 percent per year by government subsidy for a qualifying micro or small business, on facilities up to Rp500 million, with the smallest super-micro facilities set lower at 3 percent, and the government has confirmed the 6 percent rate stays even as the BI-Rate rises.

A commercial working-capital loan without that subsidy runs higher. Its rate is the bank’s published base lending rate for working capital, the Suku Bunga Dasar Kredit (SBDK, prime lending rate), plus a risk premium set for the borrower, so a business often pays in the region of 13 to 14 percent per year. Because the premium depends on the borrower, treat that range as typical rather than fixed. Those are the prices a business pays to bring money in.

The cash left idle in your account

The most common form of hidden cost is the balance kept idle for safety. A current account pays little or nothing. A term deposit pays a modest rate, and interest on a bank deposit is subject to a 20 percent final tax, so the return you keep is lower than the rate on the poster. Set that net return against inflation, which was near 3 percent in mid-2026, and idle cash in a low-paying account barely keeps its value, while cash in a current account loses ground each year. The opportunity cost of an idle balance is the return it could earn against your borrowing or in a deposit.

Now put the two prices side by side. If the same business keeps a large balance idle while paying 13 percent on a working-capital overdraft, it is paying to borrow money it already owns. The cash feels like security, and the overdraft feels like a separate problem, so the two are rarely read together. Read together, they show money leaving the business for no return. This is the pattern our team looks for first when we read a set of accounts.

The money your customers are keeping

Every unpaid invoice is money you have earned and cannot use. While a customer keeps it, that money earns you nothing, and if you are borrowing to cover the gap, it costs you the interest on the loan. The longer the average time to collect, the larger the balance permanently tied up in work you have already done.

There is a simple way to see the size of it. Take the value of your unpaid invoices at any moment, and apply the rate you pay to borrow. A business that covers Rp 500 million of unpaid invoices with a 13 percent loan pays in the region of Rp 65 million a year to finance money its customers owe. That is the upper case, since a business funding part of the balance from its own cash pays less in interest and instead gives up a return on that part.

The figures are illustrative, and the numbers for your own business come from your actual balance and rate. Shortening the time to collect, by invoicing on the day the work is done, setting clear payment terms, following up early, and charging for late payment where the contract allows, releases cash you have already earned. An early-payment discount is worth offering when the discount costs you less than the interest you would otherwise pay to cover the gap.

The money on your shelves

Stock is cash you have converted into goods. Until it sells, it earns nothing, and it can cost you storage, spoilage, obsolescence, and the interest on any money borrowed to buy it. Excess stock is a quiet drain, because it looks like a healthy, well-supplied business rather than money left idle in a store room.

The discipline is to keep enough stock to trade without interruption and no more, and to identify slow-moving lines that tie up cash for months. Money released from overstock can clear an overdraft, fund a faster-moving line, cover a tax payment without new credit, or reduce the amount you borrow at the next cycle.

The money committed too early

A fourth form is money committed ahead of need. Paying a supplier well before the goods or services are required, or ordering in larger quantities than the near-term plan supports, moves cash out of your control earlier than necessary.

Where a supplier offers a genuine discount for early payment, the question is whether that discount exceeds the return the cash could earn, or the interest it could save, elsewhere. Where there is no discount, early payment is a cost with no matching benefit.

Borrow, or use your own cash

When a business needs money for a project, the choice is usually between using its own cash and borrowing. Both have a price. Own cash has an opportunity cost, the return you give up by using it here rather than elsewhere. Borrowed money has its interest rate, whether the subsidised 6 percent of a KUR facility for a business that qualifies, or the higher commercial rate.

The test that works for both is a single one. Does the use of the money earn a return greater than the cost of the money you actually use, and greater than the next best use you could put it to. The rate in that test is the cost of the specific money in question, so it is the loan rate when you borrow and the return you give up when you use your own cash, not one fixed figure.

A project returning 8 percent a year clears a subsidised 6 percent KUR loan and adds value, while the same project does not clear a commercial loan near 13 percent, where it destroys value even while it shows a profit on the profit and loss statement, because the profit is smaller than the cost of the money that funded it.

These figures illustrate the test, and the rate that applies is the cost of your own money, which our team reads from your accounts. This is the judgement that separates a decision that looks profitable from one that is.

When the rate rises, your business pays

The price of money is not fixed. Through 2026, Bank Indonesia raised the BI-Rate by a total of 1 percentage point between May and June, to 5.75 percent, to steady the rupiah and keep inflation in range. When the policy rate rises, commercial lending rates tend to follow, so a working-capital loan or overdraft becomes dearer.

Two things follow for an owner.

- Borrowing to cover slow receivables or idle-cash gaps is dearer than it was, and the return your money needs to earn to beat its cost also rises.

- A rising-rate period rewards the owner who has already released cash from idle balances, slow invoices, surplus stock, and early prepayments, because that owner depends less on borrowing at the moment borrowing is most expensive.

Moving money across the border

For an owner with foreign shareholders, moving money out of Indonesia has its own price. From 1 July 2026, a Bank Indonesia rule requires an underlying transaction for any spot purchase of foreign currency against the rupiah above USD 10,000 or its equivalent per month per market participant, so a conversion above that level needs supporting documentation and a reason the bank can assess.

Dividends paid to a non-resident are subject to income tax under Article 26 (PPh 26) at 20 percent, reduced where a tax treaty applies. Both the timing of the conversion and the tax reduce what actually reaches a shareholder abroad, so the cost of money for a foreign-owned company includes the cost of moving it.

We set this out in more detail in our article on company reserve funds.

Roughly what this is costing you

You can estimate the drag without specialist tools. Take the money that is currently idle or tied up, meaning the balance you keep beyond a working buffer, the value of unpaid invoices, the value of slow-moving stock, and any large prepayments, and apply the cost of that money: the rate you pay to borrow for any part funded by a loan, and the return it could otherwise earn for any part that is your own cash. The result is a yearly figure for what these balances cost you, in interest paid on borrowed money and in the opportunity cost of what your own cash could otherwise earn. For many businesses the figure is larger than expected, because each balance on its own looks reasonable, and only the total shows the size of the drag.

The figure is an estimate to prompt a closer look, not a precise account, and the precise work depends on your own numbers.

How we help

Money is personal. It is the capital you built the business with, and the decisions over it affect the plans you have for the business and the people who depend on it. Our work is to translate the language of money into the decisions you actually face, so that a term like opportunity cost becomes a plain question on your own cash.

Our team reads your accounts, your collection cycle, your stock, your borrowing, and your supplier terms, and identifies where money is idle, where working capital is tied up, where the cost of funding a balance runs above its return, and borrowing could safely be reduced.. The TraceWorthy team reads the model for the pattern behind the numbers, the place where the business is quietly paying for money it already owns. From there, we build a plan to release that cash and to size any borrowing against a project that clears its cost.

If your business is profitable and still short of cash, we can review where your money is left idle and what it is costing you, and set out the steps to put it to use.

This article is general information current at the date of publication. Interest rates, tax rules, and Indonesian regulation change, and the right treatment depends on the facts of each business, so obtain advice for your own situation before you act. It is not financial or investment advice.

Frequently Asked Questions

What is the cost of money, in simple terms?

The cost of money is what you pay to have money available to use. When you borrow, it is the interest rate on the loan, so a commercial working-capital loan at 13 percent means each Rp100 million costs Rp13 million a year in interest. When you use your own cash, the cost is the return you give up by putting it into the business rather than into the next best alternative. Both are real, and both should be counted when you weigh a spending or investment decision, even though neither is shown as a line on a standard profit and loss statement.

What does the opportunity cost of money mean for my business?

The opportunity cost of money is the best return you give up by using it one way rather than another. Cash left in a current account has a high opportunity cost, because it earns almost nothing while it could reduce an overdraft, fund a profitable order, clear a supplier balance, or earn interest in a deposit. Every use of money has an alternative, and the opportunity cost is what that alternative would have returned. Reading it this way turns idle cash from something that feels safe into a decision with a price you can weigh.

Is it better to use my own cash or take a loan?

The answer depends on price and return, not on a preference for one source. Using your own cash avoids interest, though it has an opportunity cost, since that cash could earn or save elsewhere. Borrowing keeps your cash available, at the cost of the interest rate, whether a subsidised KUR loan at 6 percent or a commercial loan nearer 13 to 14 percent. The test is whether the project returns a rate greater than the money costs. A project that beats the loan rate and rewards your own capital can justify borrowing; one that does not should make you pause, whichever source you use.

How do slow-paying customers actually cost me money?

A slow-paying customer keeps money you have already earned. While the invoice is unpaid, that money earns you nothing, and if you borrow to cover the gap, it costs you the loan interest. If you cover Rp500 million of unpaid invoices with a 13 percent loan, financing them costs in the region of Rp65 million a year, and less where you fund part from your own cash. The figures are illustrative. Invoicing promptly, setting clear payment terms, following up early, and charging for late payment where the contract allows all shorten the time to collect and release cash you have already earned. An early-payment discount is worth offering when it costs you less than the interest you would otherwise pay.

How much cheaper is a KUR loan than a commercial loan?

A Kredit Usaha Rakyat loan, the government-subsidised credit for micro and small businesses, is set at 6 percent per year on facilities up to Rp500 million, with the smallest super-micro facilities lower still at 3 percent, and the government has confirmed the 6 percent rate stays even as the BI-Rate rises. A commercial working-capital loan without the subsidy runs higher, often in the region of 13 to 14 percent per year. The gap is wide, so a business that qualifies for KUR pays far less to borrow than one relying on commercial credit. Check current terms and eligibility with the lender, since these change.

How can I estimate what idle cash is costing me?

Add up the money that is currently idle or tied up: the balance you keep beyond a working buffer, the value of unpaid invoices, the value of slow-moving stock, and any large prepayments to suppliers. Apply the rate you pay to borrow, or the rate a deposit would earn, to that total. The result is a yearly estimate of what these balances cost you, in interest paid or return given up. The figure is a prompt to look closer rather than a precise account, and the detailed work depends on your own numbers.