Part of the series: Beyond Tourism

- Bali 2036: Growth Alone Will Not Protect Your Business

- Beyond Tourism: Bali Needs Waste Solutions

- Beyond Villas: Trade and Distribution in Bali

- Beyond Bali: Infrastructure and Built-Environment Services as Foreign Investment in Indonesia

- Beyond Beach Clubs: Creative Production, Events, and Destination Experiences as Foreign Investment in Indonesia

- Beyond Tourism: The Blue Economy in Indonesia – Marine and Fisheries Investment

- From Ingredient to Invoice: Food and Beverage Production as a Foreign Investment in Indonesia

- Teaching Without Permission: Lawful Entry into Indonesia's Education and Skill-Transfer Sector

- Built to Scale: Sports and Recreation Investment in Indonesia

- Clean by Design: Water Treatment, Refill, and Wastewater Enterprises in Indonesia

- The Sexiest Cow in Bali: Turning Business Waste Into a Product

Bali is still growing. What does that growth actually tell you?

Bali entered 2026 with strong recent numbers behind it. The province recorded 6,948,754 direct foreign tourist arrivals in 2025, up 9.72 per cent on the previous year. Bali’s economy grew 5.82 per cent across full-year 2025. In the fourth quarter, accommodation and food service activities contributed 22.10 per cent of provincial GRDP, the largest production-side share.

Those figures deserve a measured reading. Bali is a province inside Indonesia. Indonesia’s economy grew 5.11 per cent in 2025 across a much broader base that included manufacturing, trade, agriculture, and construction. Bali grew slightly faster, with a far narrower profile and heavier exposure to visitor-linked activity.

That difference shapes business risk. A founder arriving in Bali sees busy venues, new openings, visible construction, rising arrivals, and constant talk of opportunity. The venture can begin to feel viable before the harder work has been done. Ownership route, operating structure, cost base, reporting design, tax treatment, decision rights, and licensing sequence can all remain underdeveloped while confidence keeps growing.

A strong destination can make a weak venture look more convincing than it is. Growth gives useful context around the market. It says very little about whether a specific business has been designed well enough to trade through competition, cost pressure, uneven demand, and closer review.

“Bali’s tourism governance would shift its focus from quantity to quality.”

I Wayan Koster, Governor of Bali

Why has growth become a shortcut in founder thinking?

Strong numbers create an inviting commercial atmosphere. Foreign arrivals rose strongly in 2025. Provincial output expanded across the year. National realised investment reached IDR 491.4 trillion, about USD 29.6 billion, in the third quarter of 2025. For a founder arriving in that setting, the market can feel welcoming before the venture has been tested with enough discipline.

This reading error appears often in Bali, especially among foreign founders. Bali is often treated as if it were a country-sized economy in its own right. It is a province inside a much larger national system. That distinction affects demand, regulation, tax, banking, investment review, and the way risk should be read. A venture built around visitor demand still sits inside Indonesia’s legal and commercial setting, even when day-to-day attention remains fixed on Bali.

Founders therefore need to judge the venture separately from the destination. A busy island can still contain weak pricing, weak reporting, poor sequencing, undercosted compliance, and fragile decision-making inside individual businesses.

Can this business survive in a crowded market where volume exists and operational pressure intensifies?

Bali’s recent data already describes a market with strong traffic and uneven trading conditions. In March 2025, direct foreign arrivals reached 470,851, up 4.47 per cent from February. In that same month, the room occupancy rate for star hotels fell to 46.61 per cent from 51.62 per cent in February, and sat 6.10 percentage points below March 2024. Across full-year 2025, Bali’s economy still grew 5.82 per cent. Accommodation and food service activities remained the province’s largest production-side contributor, reflecting how much business activity still sits close to visitor demand.

For an operating business, that combination has immediate consequences. Pricing comes under strain as more operators compete for the same customer pool. Softer occupancy or turnover affects staffing, purchasing, service consistency, and cash planning. Management needs usable numbers early in the month because a busy destination does not guarantee an easy month inside the business.

Pressure usually shows up first in payroll, supplier payments, discounting, founder over-involvement, and reporting that arrives too late to guide decisions.

The founder needs workable answers to three questions.

- Can the business carry staffing and service costs through weaker trading periods?

- Can pricing absorb competitive pressure without damaging the concept?

- Can management see revenue, cost, and cash movement early enough to respond in time?

Businesses with thin reporting, vague internal responsibility, and optimistic cost assumptions usually feel this strain first.

Does this venture have the structure and discipline to win in a more selective environment?

Bali can stay busy while the business environment becomes easier to read. More of the commercial trail can now be checked through payments, reporting, agreements, tax records, licences, and day-to-day operating conduct.

Indonesia’s payment system is one sign of that shift. By the first half of 2025, QRIS had reached 57 million users and 39.3 million merchants, with 6.05 billion transactions worth IDR 579 trillion. A larger share of business activity now moves through channels that are easier to trace, compare, and question.

Different counterparties read different parts of the venture. Guests notice reliability, booking experience, payment ease, and dispute handling. Investors notice ownership route, agreements, reporting discipline, and whether the numbers can be followed without too much explanation. Regulators notice licences, tax reporting, staffing arrangements, and whether the declared business activity matches what is happening on the ground. Commercial partners notice whether the venture is documented properly and managed in a way that supports consistent performance.

Weak set-ups become commercially awkward here. Documents may have been assembled at different times for different immediate needs. Revenue may be moving through a structure that no longer fits the operating model. Tax treatment may reflect an earlier version of the venture. Reporting may exist, though not in a form that lets a third party understand how the business actually earns, spends, approves, and decides.

A venture becomes easier to assess when ownership route, agreements, payment flow, licences, reporting, and tax treatment describe the same business. That affects banking, investor confidence, partnerships, expansion planning, and the ease with which the venture can answer ordinary commercial questions.

Can this venture absorb variation in revenue, regulation, and investor sentiment?

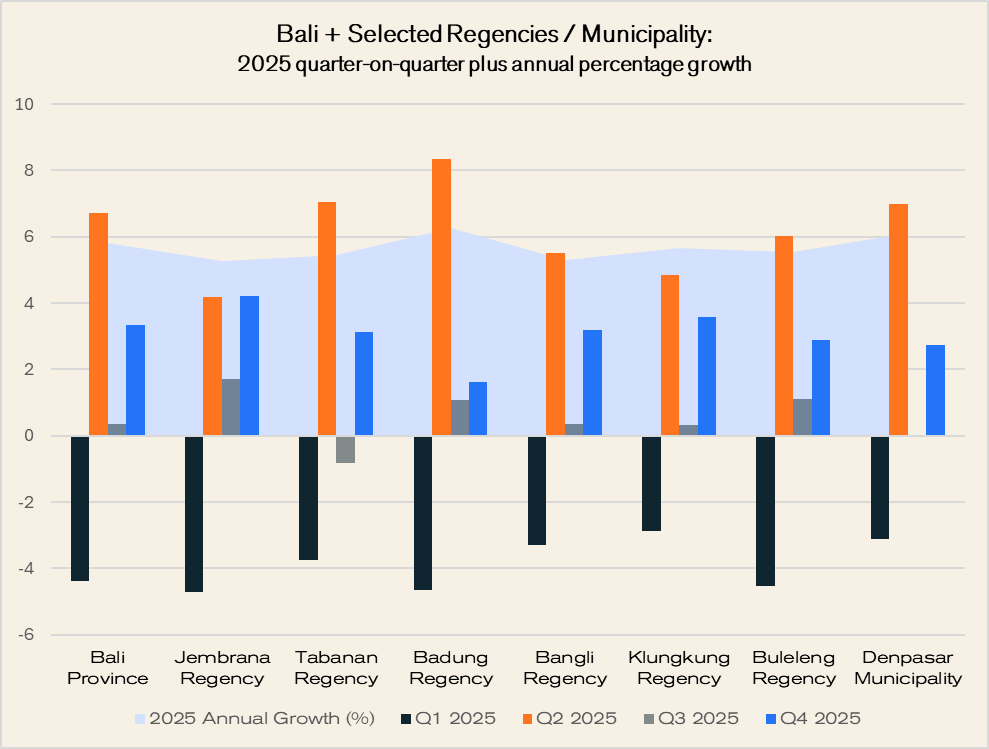

Bali’s economy expanded 5.82 per cent across 2025, while fourth-quarter growth reached 5.86 per cent year on year and 3.33 per cent quarter on quarter. The province-wide figure is useful, though it smooths over local variation. The chart below and the data table at the end of this article show a more uneven year across selected regencies and Denpasar.

Badung accelerated strongly in the second quarter, then eased. Tabanan moved into contraction in the third quarter before recovering. Denpasar lost momentum sharply in the third quarter and improved later in the year. Forecasts built on one smooth market story are too neat for the conditions Bali actually recorded.

Revenue is the first pressure point. If sales arrive later than forecast, the business still needs enough room to cover payroll, rent, supplier commitments, tax obligations, platform costs, and management overhead. A model that only works when revenue lands on time and near target is thin from the beginning. The early months need margin for softer demand, slower customer build-up, discounting pressure, and seasonal movement between locations and customer groups.

Regulation is the second pressure point. Some delays are administrative. Others change cost, timing, staffing, or the order in which the business can expand. If the venture depends on business licences, sector-specific approvals, imported equipment, land use alignment, staffing documents, or platform eligibility, delay affects more than the launch date. It can force re-sequencing, increase carrying costs, and expose whether the original model was too optimistic about how quickly the business could begin earning properly.

Investor sentiment adds another layer. Funding conversations can begin warmly when Bali itself feels persuasive. That mood can cool once investors ask for stronger governance, staged deployment, more conservative forecasts, or clearer evidence of lawful operating design. A venture with discipline can respond by narrowing scope, preserving cash, opening in phases, or postponing expansion without losing direction. A venture built around perfect timing and uninterrupted backing has far less room to adjust.

This part of the review needs direct answers. How quickly does the business become uncomfortable if revenue arrives in waves. How much working capital sits between a manageable month and a difficult one. How exposed is the concept to one customer group, one season, or one price point. How much strain lands on the founder when several moving pieces change at the same time.

The budget should show what happens if revenue lands below plan for several months. The operating plan should show which costs can move and which cannot. The regulatory pathway should show where delay is possible and what commercial effect follows. The capital plan should show whether the business can continue through a slower start without immediate dependence on fresh money or unusually patient investors.

Would the current business set-up still make sense if scrutiny increased?

Bali can stay attractive while becoming more demanding.

That is a normal feature of a maturing destination. More money moves through formal channels. More business activity leaves records that can be compared. Ownership route, tax treatment, licensing, payment flow, staffing, and day-to-day conduct become easier to read alongside each other.

QRIS adoption is one sign of that shift. A larger share of commercial activity now moves through systems that are easier to trace and review. For a founder, the practical question is simple. Do the papers, the operating activity, and the money flow describe the same business.

That question needs to be tested from several directions. A bank reads account activity and source of funds. An investor reads ownership, agreements, reporting discipline, and decision rights. A regulator reads licences, tax reporting, staffing, and whether the activity on the ground matches what has been declared. A platform or commercial partner may only see one part of the venture, though that can still be enough to expose inconsistency.

Weak design usually appears through mismatch. The licence describes one activity while revenue is earned in another. Agreements were prepared at different times for different immediate needs and no longer fit neatly together. Tax treatment still reflects an earlier version of the venture. Monthly reporting exists, though not in a form that lets a third party follow how the business earns, spends, approves, and decides.

The set-up deserves close reading before somebody else provides it. If a new investor reviewed the venture today, would the ownership route read coherently. If a regulator compared licences, staffing, contracts, and actual trading activity, would the same picture appear. If the business needed banking support, fresh capital, or restructuring, would the present design help the process move forward.

Some ventures drift into this problem gradually. The business opens quickly, adapts as opportunities appear, and adds documents in stages. Daily trading can continue, though the venture becomes harder to explain once several counterparties begin reading different parts of it at the same time. Expansion, funding, partnership discussions, and exit planning all become more difficult when the business cannot be described cleanly from ownership through to revenue.

A sound set-up should still read sensibly when examined from several directions at once. The legal structure should fit the activity. The agreements should fit the operating model in use. Reporting should explain how the venture earns, spends, pays, and decides. Tax treatment should follow the commercial reality of the business now being run.

What should be tested before capital is committed?

By this stage, several questions should already have answers.

- Does the venture still work when trading is softer for several months?

- Does the cost base still make sense once compliance, tax, reporting, and lawful operation are fully priced in?

- Does the structure fit the actual activity, location, staffing pattern, and transaction flow?

- Can the founder explain ownership, approvals, agreements, reporting, and tax treatment as one coherent venture?

- Can the business continue if approvals move slowly or investors ask for a narrower first phase?

- What management information will need to be reviewed each month once the business is live?

Those questions shape the decision on whether the venture is ready for capital.

How much governance does this venture need before it starts operating?

Enough that the business can decide, spend, contract, report, and respond in an orderly way from the first day of trade.

That usually means a settled position on authority, ownership, reporting rhythm, contract discipline, approval sequence, and escalation when revenue misses plan, costs rise, or one approval slips. Who can approve spending. Who can sign agreements. Who reviews monthly numbers. Which approvals must already be in place. Which part of the structure receives income, carries cost, and bears risk. Who responds when revenue misses plan or one approval slips.

What structure will this venture actually need to operate responsibly?

Who is investing. Through which lawful route. Into what entity. For what real activity. In what location. With what management arrangement. With what tax consequence. With what reporting burden.

A responsible operating structure usually starts with six linked decisions.

- The legal vehicle must fit the activity.

- The licensing pathway must fit the way revenue will actually be earned.

- The tax treatment must fit the transaction flow.

- Authority inside the business must be allocated to named people.

- Reporting must begin from the first period of operation.

- Contracts must match the commercial model in use.

Different ventures will need different arrangements. A single-site hospitality business, a service company with foreign management, a property-linked income model, and a multi-entity investment arrangement do not belong inside the same template. The right structure depends on the activity, the investment route, the approvals required, the reporting burden, the tax consequence, and the way control is actually exercised.

Weak design usually appears later through avoidable problems. Revenue enters through the wrong place. Approvals do not match the activity on the ground. Tax treatment reflects a simplified version of the business rather than the one now trading. Contracts describe relationships that no longer match the operating model. Expansion then becomes slower, banking conversations become harder, investor review becomes heavier, and correction work becomes more expensive.

Before launch, the founder should be able to describe the venture in one clean sequence: who is investing, through which lawful route, into which entity, for which activity, with which approvals, under which management arrangement, with what reporting burden, and with what tax consequence. When those answers fit together, the venture is far easier to run responsibly in Bali.

What should feasibility work test before a founder commits money?

Serious feasibility work should test how the venture performs under ordinary commercial pressure.

Projected revenue is only one input. The review should also examine slower trading periods, labour cost, fit-out timing, tax exposure, licensing sequence, reporting duties, management capacity, reserve needs, and the extent to which the business depends on the founder’s direct involvement. The monthly operating rhythm belongs in that review as well. A venture can appear profitable across a full year and still create strain within particular months.

Bali’s 2025 data supports that approach. Provincial growth was strong, though quarterly movement and local conditions were uneven. Tourism activity, occupancy, and local growth patterns did not move in one smooth line. A founder planning from a single growth narrative is likely to overstate demand, understate pressure, or miss the effect of timing.

The feasibility review needs direct answers to a short set of questions.

- How long is the path to stable operations?

- What does the cost base look like once compliance, reporting, and lawful operation are fully priced in?

- What changes if an early trading assumption misses?

- How many months of weaker trading can the venture absorb before cash becomes tight?

- What management information will need to be reviewed each month once the business is live?

The review should identify where the venture is most likely to come under strain, how early that strain may appear, and whether the expected return still justifies the capital under consideration.

Who helps founders assess all of this before capital is committed?

Founders rarely receive one neat answer at the beginning. They usually receive fragments. An agent may speak to location or land. A lawyer may address formation or agreements. An accountant may explain tax reporting. Another operator may describe what worked in a different business, at a different time, in a different part of Bali.

The difficulty sits in the gaps between those fragments. Advice can be partially right and still be wrong for the venture being built. Timing can be wrong. Sequencing can be wrong. One technical answer can create a problem somewhere else in the model.

Founders need one process that reads the venture as a whole. Structure, licensing, tax, governance, reporting, feasibility, and operating method affect the same business. Reading them together gives the founder a stronger basis for deciding whether to proceed, reshape, phase, or pause.

This is also the stage where revision costs least. Ownership route can still be reconsidered. Licensing pathway can still be matched to real activity. Budget can still be tested against softer revenue or delayed approvals. Internal authority and reporting can still be designed before confusion becomes routine.

TraceWorthy brings those legal, tax, financial, compliance, immigration, structuring, and operating questions into one decision process when a founder is preparing to commit capital in Bali.

What will prepared operators still be doing well in Bali ten years from now?

Prepared operators are likely to keep doing the ordinary disciplines well. Their economics will still work in a market that feels less forgiving than the launch story suggested. They will know their cost base, customer mix, reporting rhythm, and decision structure. Banks, investors, regulators, and commercial partners will find the venture easier to understand.

They are also likely to read Bali more carefully. Local variation will still affect demand, staffing, pricing, and expansion choices. Operating pressure, regulatory movement, and slower capital will still need room in the model. Governance will still need to function inside daily business life rather than arriving later as repair work.

Ten years from now, the stronger operators are likely to be the ones whose ventures were examined properly before capital went in.

TABLE: Bali and selected regencies / municipality: 2025 quarter-on-quarter growth and annual growth

| Area | Q1 2025 (%) | Q2 2025 (%) | Q3 2025 (%) | Q4 2025 (%) | 2025 Annual Growth (%) |

|---|---|---|---|---|---|

| Bali Province | -4.38 | 6.70 | 0.34 | 3.33 | 5.82 |

| Jembrana Regency | -4.71 | 4.17 | 1.71 | 4.22 | 5.26 |

| Tabanan Regency | -3.73 | 7.06 | -0.81 | 3.12 | 5.45 |

| Badung Regency | -4.64 | 8.35 | 1.09 | 1.61 | 6.26 |

| Bangli Regency | -3.29 | 5.51 | 0.35 | 3.19 | 5.31 |

| Klungkung Regency | -2.86 | 4.86 | 0.31 | 3.58 | 5.67 |

| Buleleng Regency | -4.54 | 6.01 | 1.12 | 2.88 | 5.54 |

| Denpasar Municipality | -3.11 | 6.97 | 0.02 | 2.73 | 6.11 |